With increasing competition and demand for top talent and best-in-class employees across all functional levels of insurance carriers, talent is a hot topic across the industry. Executive and manager-level calendars are filled with meetings focused on hitting agreed upon goals from 2016. Efforts to attract, engage, and retain new and existing staff are being re-energized. Determining which initiatives will provide the biggest boost is a key.

Competition is High

As we move into 2017, mutual insurance companies find themselves in a highly competitive market. The most critical issues for insurers are finding the right talent and access to capital and technology. At the end of the day, talent represents the highest cost, yet greatest asset of most firms.

We all know that cost is a necessary component of doing business, with salary and benefits proving to be insurers' highest cost outside of sales commissions, at typically 13% of revenue. These costs are only expected to increase in the foreseeable future. Reflecting the increased need for highly skilled talent and desire for employee growth, firms are seeing employee training costs have increased by 44% since 2013, costing insurers $606 per full time employee each year. For those firms looking to hire staff with specific technology, actuarial, or analytical skills, the costs are even higher.

To be successful in the current market, insurers have to understand and strengthen efforts to reach today’s consumers. They must recognize that millennials have changed the playing field and find ways to effectively engage and utilize this talent pool. At the end of the day, insurers must determine whether they have the right people in the right positions to ultimately drive the firm and business initiatives. As the highest increasing segment of the workforce, capturing the hearts and minds of millennials is key to their success.

With or without hiring strategies in place, recruiting will remain a significant challenge for insurers. For the first time ever, the percentage of employees over the age of 60 is roughly equivalent to that of the percentage of millennials. This makes hiring for succession even more challenging, as the rate of retirement for the 60+ cohort accelerates. When planning to hire for innovation, property-casualty insurers should start to look beyond the insurance industry for talent. Interestingly, 85% of organizations with a diversity-focused staffing strategy, report increased performance as diversity is shown to drive creativity, innovation, and fosters a culture of adaptability and productivity.

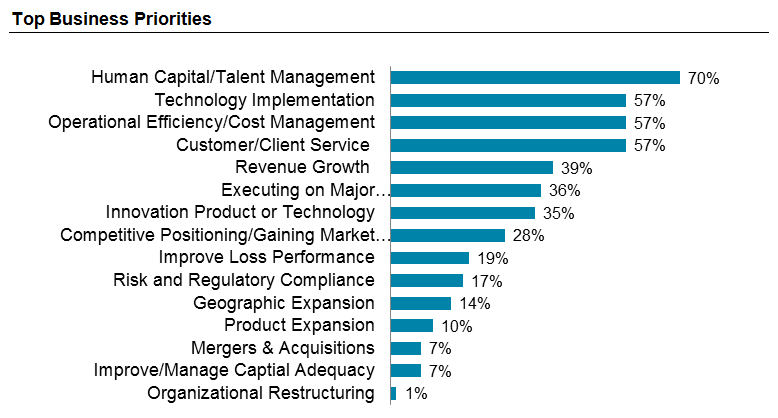

In our recent Human Capital Strategy Assessment Survey, conducted from May-July of 2016, we saw that insurers' human capital priorities emphasize the importance of human capital / talent management at a rate of 70%.

With this overwhelming report of human capital / talent management being a top priority, the next question is how do insurers rate the effectiveness of their current programs?

In the recent survey, the majority of respondents considered their firm’s benefits, compensation, retention efforts, culture, and recruiting efforts to be effective, highly effective, or exceptionally effective. Worth noting, however, is that more than half reported Opportunity for Improvement in the areas of human capital analytics, career pathing/mobility, succession planning, leadership & development, and diversity / inclusion.

While the human capital programs were primarily considered effective by insurers, they were not considered to be highly supportive of, or even aligned with, strategic business priorities. In fact, only 40%-52% of respondents rated their top five most effective human capital programs as highly or completely supportive and aligned. Those percentages dropped dramatically, down to 7%-29%, for their programs ranked as least effective programs.

To drive operational efficiency, HR processes must be linked to firms’ current and future business objectives rather than operate as a silo within the organization.

Meeting future business needs requires strengthening existing capabilities along with focusing on operational efficiency. Formalizing a well-defined human capital strategy is an integral part of this initiative. Activities such as building talent pools to feed the leadership pipeline, enhancing the organizational culture, increasing diversity across all levels, and ensuring there are change management processes and capabilities in place are important starting points for any organization.

There is a critical opportunity for insurers to invest in and leverage human capital analytics. Having the ability to mine and manage all of the data that carriers have available to them is an important step toward operational efficiency.

Think of a crew team. Even if everyone knows how to row, where the finish line is, and is in top physical condition, but their efforts are not aligned, the boat will go in circles.

Of course, talent management and succession planning are key issues across all industries. But, within insurance, and other regulated industries, there are now external pressures on these companies. This has upped the ante and broadened involvement beyond senior management right up to, and including, the board of directors.

Insurers can get started by beginning or continuing to plan, develop talent, introduce and utilize organizational analytics, train employees, focus on culture, and engage staff. But they must also stop relying on manual or outdated processes that rely on paper exchanges, old technologies, or rigid and static performance evaluations.

A well planned and advised investment in talent can make all the difference. Aligning human capital processes with business goals requires understanding both short- and long-term priorities.

To watch a recent webinar on this topic, please click here.

If you’d like to explore how to align your talent strategies to your company performance, get help recruiting the right talent, or update your performance management systems, please contact our team.

Related Articles