Most banks use peer groups to evaluate their executive compensation programs. However, since every peer group process is unique, creating hard and fast rules is not usually the best approach for firms to take. We have seven questions for consideration that may change the way you think about your compensation peer group altogether.

1. Is asset size the right measurement of size?

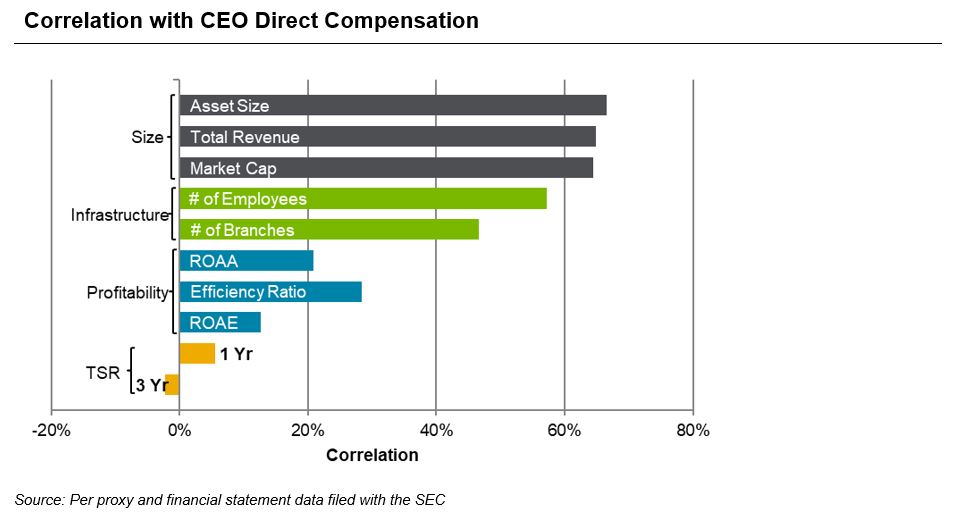

Organization size is the most important predictor of executive compensation within the banking industry, as the chart below demonstrates. However, the relevant measures of firm size go beyond just total assets.

For banks that have outsized non-balance sheet business lines, such as private banking, trust, mortgage, and financial advisory, asset size only captures a portion of the overall size of the organization. If you are one of these banks, consider using a broader measure, such as annual revenue, to better reflect the true size and complexity of your organization.

2. What is the most accurate time period to use in order to evaluate size?

Most banks tend to look at current size to identify potential peers, but that is not necessarily the best tactic. Remember that proxy compensation data is backward-looking. It is critical to know how big your peer banks were at the time they filed their proxy. This is important because a bank that is comparable to yours in its current size could have grown recently, which means that its proxy data reflects compensation decisions made when it was a much smaller organization. For example, if a potential peer is currently $15 billion in assets, but was $11 billion at the end of the previous fiscal year, the compensation data the firm reports will most likely reflect its smaller size.

Current and future size is a chief consideration if you plan on using the peer group for performance comparisons. To account for potential changes, we use a simple pro forma calculation based on planned acquisitions in order to estimate a firm’s future size.

3. How should you think about location?

Location can be a significant consideration in peer groups, but its true definition may be different than what you expect. In some cases, the characteristics of each bank’s specific market are more important than the actual geographic location within the country.

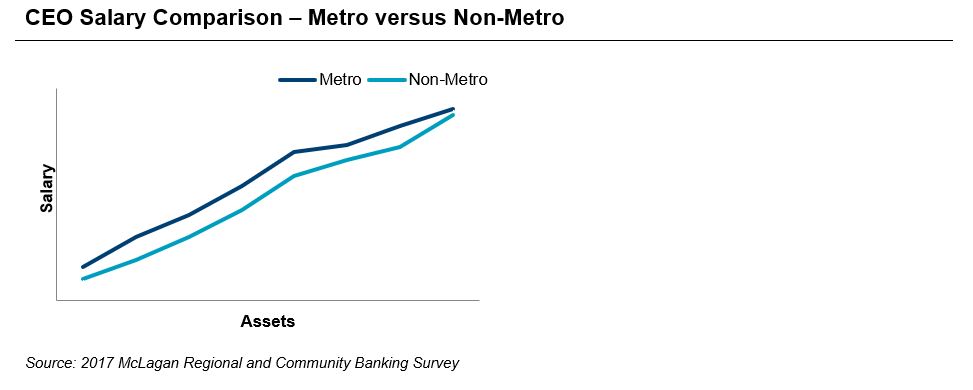

The below analysis compares CEO salary and firm asset size. The blue line represents CEOs at banks in the 50 largest metro areas, while the grey line represents CEOs at banks located outside of top-50 markets.

As you can see, CEO compensation differs significantly between banks in a top-50 market and banks in smaller areas. CEOs in metro locations earn a 10% higher salary on average than those in non-metro locations.

Not all banks are able to use location to define their peer group. However, if you do, consider thinking beyond what’s right next door.

4. Should you filter for business mix?

While it may seem counterintuitive, business mix actually does not have as much of an impact on executive compensation levels as you might think. Whether looking at commercial versus consumer focus, banks versus thrifts, or traditional banking versus specialty businesses, we don’t see significant differences in executive compensation as long as the organization size is properly scoped.

However, business mix can have a great impact on performance. You may choose to consider business mix more carefully if you intend to use peer groups to formally measure performance.

5. What role do bank financials play?

It is useful to understand the nuances of banking financials when reviewing performance against your peers, both informally and as part of formal performance plans. For example, what are the unique factors potentially impacting both your and your peers’ financials? Is your profitability best measured through return on assets, return on equity, or return on tangible equity? How should you consider the impact of write downs of deferred tax assets in 2017 on profitability performance? How should you handle potential peers reporting a 2% return on assets?

All in all, it’s critical to make sure that your management team, your committee, and your compensation advisors understand and have considered how the story behind the numbers impacts peer group selection.

6. Should you look at compensation as part of the peer selection process?

Potential peers sometimes have unique compensation situations that are not representative of typical market practice. While we do not recommend basing peer selections on compensation levels or program features, there are three significant outlier situations to look for:

1. Does the company have significant inside ownership, particularly by management? If so, the bank sometimes will have different trading patterns or a different management focus than most banks. Executive compensation in these situations is also subject to different market forces than at most public banks and, as a result, may not be representative of typical practices.

2. Has the bank gone through a mutual conversion in recent years? Newly converted banks often make significant up-front equity grants to management followed by a period of infrequent or no equity grants. This unique equity pattern makes direct market comparisons more complicated.

3. Is the bank subject to a regulatory enforcement action? Severe regulatory enforcement actions can sometimes impact executive compensation levels. Know how to identify these banks and consider carefully whether they will serve as strong comparison points for your compensation plans.

7. Should your process be the same as that of ISS and Glass Lewis?

ISS and Glass Lewis have their own peer group selection procedures that are based on their need to review thousands of public companies. For public banks, it is appropriate to identify your own set of relevant criteria rather than relying on the processes of shareholder advisors. However, it is still important to understand how the advisors select peer groups, how and why it differs from your selection procedure, and how this can lead to a different assessment of compensation and performance.

Glass Lewis in particular uses a peer-of-peer approach to peer grouping that can result in compensation data that trails the bank’s current size by more than a year. At a minimum, you will want to know how your peer group does or does not overlap with that of ISS and Glass Lewis, so that there are no surprises when they issue their recommendations prior to your annual meeting.

Peer groups seem simple to construct at face value, but without carefully thought-out plans, peer group decision-making can result in groups that lack relevance or are not representative of industry practices. Asking yourself the right questions will help you craft more effective compensation peer groups now, and in the future.

For more information on effective peer group selection for banks, please contact our team.

Related Articles