When considering sales incentive design practice among life insurers, the chorus from Fiddler on the Roof may come to mind—Tradition...Tradition...Tradition. While traditions can provide some consistency and comfort, at what point do we have to seriously reconsider and revamp incentive design practices? At what point do we have to ask, does it really make sense to keep doing it this way?

A key challenge may be maintaining objectivity when assessing even very fundamental sales incentive design questions, e.g., salary or draw, commission or bonus, formulaic or discretionary, and heavy or limited leverage. A helpful way to obtain some objectivity is to examine the core attributes of the given sales role irrespective of the specific business, while also assessing how similar roles are paid in the broader general industry market, beyond simply insurance or even financial services. With this approach in mind, in this article we highlight some select sales roles in the life insurance industry that illustrate the extent to which life insurers may be continuing to go their own way, albeit, perhaps for the sake of tradition.

Insurance sales methods and roles

Overall, there are a variety of ways that insurance company products are sold. Companies can sell individual products via independent agents, captive agents, the internet, or direct mail. Additionally, companies can distribute group insurance products via agents to employee or association groups. With these sales methods, there are a wide range of roles involved, many with unique characteristics that are worthy of consideration when assessing pay design. Further, there are a myriad of factors that influence pay design for these insurance industry roles, as well as any industry sales roles. Some key factors that could influence virtually any sales role pay design include:

Below we highlight aspects of a sampling of insurance sales roles, dissecting the roles to see what might be expected across general industry:

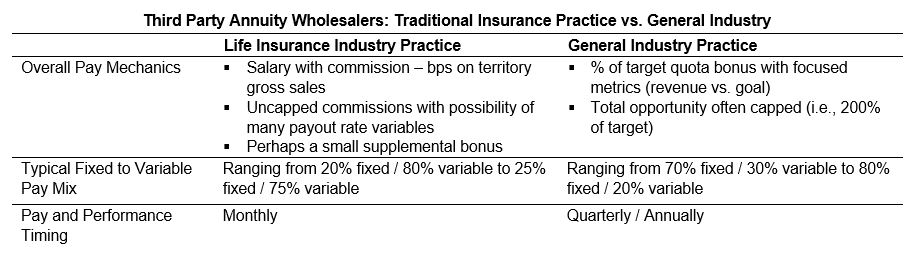

Third Party Annuity Wholesalers

Third party annuity wholesalers are responsible for promoting product sales among assigned independent agents or brokers in an allocated territory. Overall, they focus on developing relationships with independent reps, educating reps on the benefits of their company’s annuity products, and coaching reps on how to identify opportunities to help their clients. As shown below, these wholesalers typically receive a base salary and a commission on all territory gross sales, as well as possibly a smaller supplemental bonus. Under this arrangement, the role is highly leveraged. For example, 20% fixed salary and 80% variable incentive. For general industry positions like this that are not directly involved in the actual client sale, the incentive is usually a target bonus that might be capped on overall opportunity. Additionally, we would anticipate such a role to not be as leveraged as it is in insurance practice.

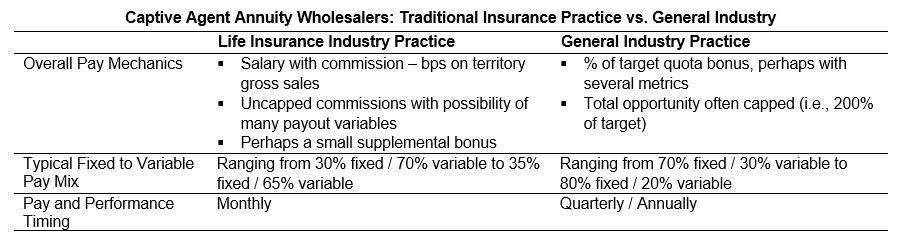

Captive Agent Annuity Wholesalers

This role is similar to third party annuity wholesalers in that the individual is responsible for promoting annuity business in a territory. The difference in this case is the wholesaler’s target audience is reps who are fully aligned with the wholesaler’s parent company. Thus, the captive agent wholesaler does not have to compete for shelf space in the way that a third party wholesaler does. Therefore, it behooves the captive agent to listen to their wholesaler, since they are ultimately there to help them sell. Interestingly, pay design practices for this role are often similar to that of third party annuity wholesalers, even though the role is arguably more of a product specialist in nature, versus a sales role. Given its unique dimensions, we would see even more of an argument for a general industry practice—target bonus incentive with an overall pay package that is not overly leveraged.

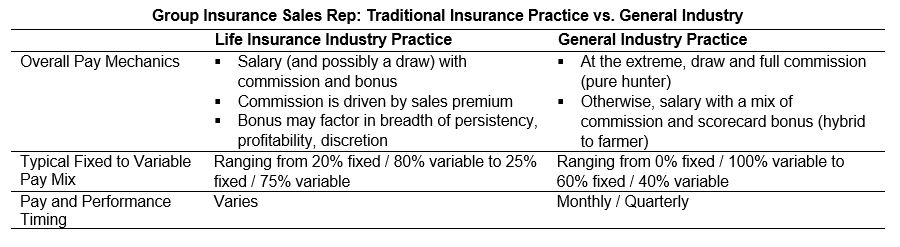

Group Insurance Sales Rep

While group insurance sales reps often work through agents, as a wholesaler does, they typically play a much more involved role in selling to the ultimate customer—a B-to-B sale that is relatively complex with a long sales cycle. Sales design practices for this role typically involve a salary with a possible draw and a mixed incentive that involves a commission and target-based award that could include discretion. Examining industry practice for this role is a bit more nuanced, as it depends on the extent to which the incumbent is a hunter versus a farmer. At the extreme of a hunter, one might almost argue for a design that is based on 100% commission. In true practice, most companies’ group sales roles contain a blend of roles and hence we would expect to see a mix of salary, commission, and bonus, with a more balanced approach to leverage.

| Group Insurance Sales Rep: Traditional Insurance Practice vs. General Industry |

| |

Life Insurance Industry Practice |

General Industry Practice |

| Overall Pay Mechanics |

- Salary (and possibly a draw) with commission and bonus

- Commission is driven by sales premium

- Bonus may factor in breadth of persistency, profitability, discretion

|

- At the extreme, draw and full commission (pure hunter)

- Otherwise, salary with a mix of commission and scorecard bonus (hybrid to farmer)

|

| Typical Fixed to Variable Pay Mix |

Ranging from 20% fixed / 80% variable to 25% fixed / 75% variable |

Ranging from 0% fixed / 100% variable to 60% fixed / 40% variable |

| Pay and Performance Timing |

Varies |

Monthly / Quarterly |

Why Break Tradition?

Our comments above are not to say that industry-specific market intelligence isn’t important. Industry practice is particularly crucial with respect to recruiting and retention. Like everyone, salespeople talk and are attracted by incentive designs that are consistent with what they hear are industry norms. Stated simply, having an industry-competitive incentive makes your company’s sales pitch that much easier to convey when trying to appeal to talent. But, industry-specific practice shouldn’t be your only input for plan design, particularly when the business has changed and past traditions may no longer apply. Your company’s sales incentive practice should ultimately reflect what makes sense for the role, such that it is aligned with the pay philosophy and operating goals of the business and your overall organization.

To learn more about incentive design strategies for life insurance companies, please contact our team.

Related Articles