If you mentioned to the average person in 2006 that you worked in compensation, it was likely that they either had no idea what you meant, or perhaps assumed that your role somehow involved worker’s insurance associated with accidents or injuries. Since 2008, the world has become much more aware of – and fascinated with – the concept of compensation. The initial focus was on executive compensation, but over time, topics like gender pay equity and minimum wage have become everyday conversations. While these are all important issues and worthy of attention, many of these topics elicit emotional responses and lack grounding in what truly drives pay.

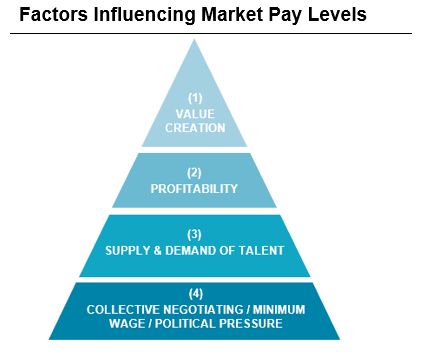

Assuming that pay is working properly, there are a few factors that typically drive pay levels in the broad market:

- Supply and demand is frequently paramount—how many people have the skill relative to how many companies require it. This is a basic underpinning of all pay levels. Compensation can often reflect a surprisingly efficient market. For example, there is high demand for fast food workers, but a seemingly matched supply of talent, so wages tend to be low.

- Another factor is the value creation associated with a role. In general, roles that create more value or have more perceived impact tend to be compensated better. There is a modest demand for investment bankers and a meaningful supply of people who aspire to that role. However, the value created from the role is high, so the pay tends to be correspondingly high.

- Industry / company profitability plays a large role in determining pay levels, too. Consider financial services—an industry that was far more profitable in 2006 vs. 2018, where diminished profits have reduced pay levels, overriding supply and demand concerns.

- Several other public factors may help determine pay levels. Collective negotiating can influence pay materially in some geographies and business areas, though this has waned over time. A society’s overall desire to set a baseline quality of life for workers also influences absolute pay levels, but perhaps not as much as it should. Lastly, political pressure can impact pay materially, as seen in some countries where strong restrictions on executive pay levels create surprising variances from the same positions in other geographies.

While the story of pay for control functions is one that interacts with some of this reward theory, it also speaks to the idea of aggregate vs. per capita pay, which we will discuss further below.

In the run up to the financial crisis, we saw pay levels for revenue producers – investment bankers, fixed income traders, etc. – grow quickly, placing a huge amount of distance between their rates and those of compliance, finance, and risk management staff. The primary driver of this disparity was perceived impact / value creation. There was a high demand for quality bankers and a reasonably high supply. There was a low demand for quality compliance, audit, and risk management staff and a reasonably low supply—it was in balance. However, the perceived impact / value creation for bankers and traders was through the roof. In hindsight, it would be easy to say that the perceived value of compliance, finance, and risk management was underestimated.

Post crisis, we have seen pay rates come down for all roles—more dramatically for bankers and traders at first. The demand for control functions talent has accelerated based in part on the regulatory environment, but also by boards of directors and CEOs wanting to ensure that their firms are taking adequate precautions. A fascinating indicator of perceived impact is reporting level. Consider that a Head of Compliance in 2006 may have reported to the Head of Legal, who may have reported to the Chief Operating Officer, who may have reported to the CEO. It is not uncommon to see a Compliance Officer now have a meaningful seat at the table. Additionally, Heads of Audit now frequently have a direct report into the Board of Directors. The industry clearly believes that these areas have great impact and create value.

From a supply and demand perspective, these people remain hard to find. As firms across financial services have deepened their concerns around control, consulting firms have become a meaningful employer of people with control function expertise, enabling them to bid up the cost of talent. Yet, despite this wide demand, per capita pay has not increased back to pre-crisis levels.

Aggregate pay, on the other hand, tells a completely different story. While there is great value in per capita benchmarking of pay, in many instances – this one in particular – the benchmarking of aggregate pay may create exponentially more value. Consider a firm that is 30% understaffed in their control functions, but pays 5% above the market on a per capita basis. Without benchmarking the aggregate pay, a firm may be inclined to spend even less in this area, when in fact, their gap to market may be a good indicator that the firm is not adequately addressing important risk issues.

Similarly, a firm that pays below market on a per capita basis and is relatively close to market benchmarks for overall staffing levels might feel confident that costs in these areas are well under control. However, if their mix of resources skews heavily towards senior, experienced staff and/or higher cost roles within the functions, it will drive aggregate spend levels well above market. This can be the result of a more complex business mix that requires greater experience and specialization, or simply an opportunity to improve efficiency.

As we look at the scale of these functions, we most often find value in considering the relative size and cost rather than the absolute size. Firms benefit from looking at things like control functions headcount as a percent of overall firm headcount, comp spend in the control functions as a percent of overall comp spend, control functions comp spend as a percent of revenue, etc. Once measured at the overall control functions level, it is useful to drill down into compliance, finance, audit, risk, etc. and perform a similar analysis. Within these groups, one can explore mix of seniority, per capita pay, seniority / reporting level of leadership, spans and layers, and more to determine how structure drives the overall spend and whether any observed variances in structure are warranted by unique aspects of their business or not.

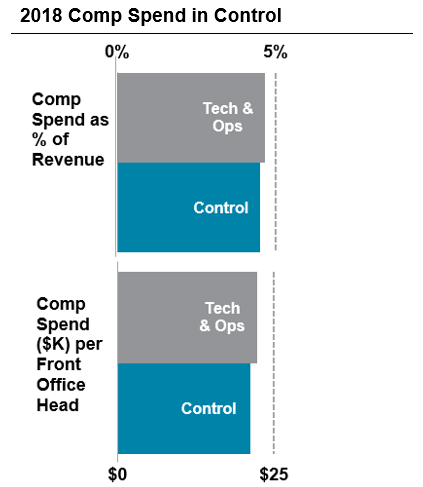

Given that comp spend in the control functions for the average bank rivals its spend in technology and operations, it is more critical than ever to ensure that the aggregate investment in these areas is appropriate and that those dollars are spent wisely.

Firms that have done this thorough analysis can have greater confidence that they have appropriately resourced themselves to guard against risk and other challenges. Rewards leaders who initiate and conduct this work now have a proper seat at the table with both the Boards of Directors, as well as various regulatory bodies in ensuring that the firm is market competitive in how it staffs and rewards groups tasked with such an important concern for the enterprise.

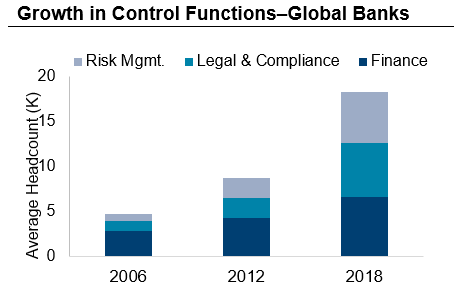

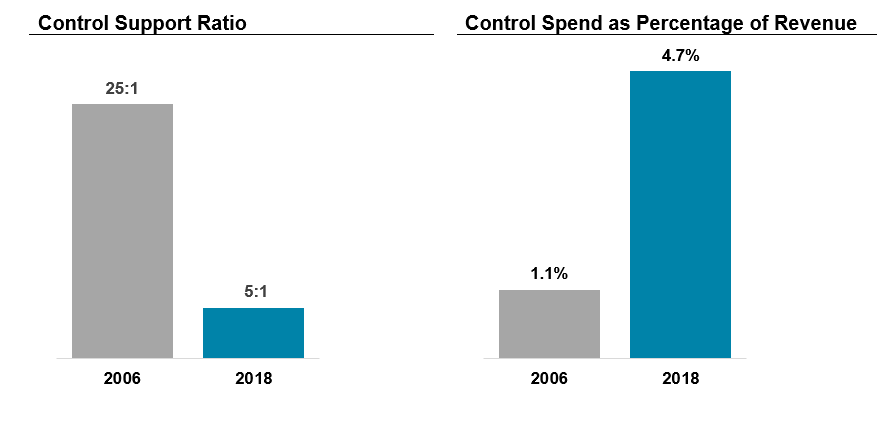

Over time, we have seen the aggregate cost of these groups skyrocket, with finance headcount among large banks growing at an annual rate of 7% since before the crisis. Risk management and compliance functions have experienced double-digit annualized growth. The number of employees supported per control function head dropped from 25 in 2006 to 5 in 2018, while the cost of compensating the control functions grew from 1% to almost 5% of firm revenue.

This remarkable growth illustrates that comparative analysis isn’t only intended to verify that firms are spending enough—in some cases, it is just the opposite. A number of firms, full of good intention and possibly a legitimate need to bolster their defenses, may have meaningfully overshot either reasonable or sustainable levels. These organizations can use comparative analysis to pinpoint areas of excess and build a remediation strategy.

While per capita pay rightly will stay front of mind, and the factors described earlier will continue to drive pay levels across the industry, we expect firms to put increasing emphasis on aggregate benchmarking. Those that do will have a decided advantage in ensuring that pay levels and staffing are important elements of a coherent human capital strategy for their control functions.

To learn more about aggregate pay benchmarking and compensating control functions in financial services, please contact our team.

Related Articles